The Power of Investing: How to Grow Your Wealth Over Time

Earning money is one thing. Growing it is another. Millions of hardworking people spend their entire lives earning a salary, yet retire with little to show for it. The reason is simple — they never learned to invest. They saved in bank accounts, watched inflation quietly eat away their purchasing power, and missed decades of potential wealth creation.

Investing is not gambling. It is not reserved for the rich. It is a disciplined, proven process that allows ordinary people to build extraordinary wealth over time. This article breaks down the world of investing in plain, simple language — what it is, why it matters, and how you can get started today.

- WHY SAVING ALONE IS NOT ENOUGH

Let us start with a hard truth: money sitting in a regular savings account is slowly losing value.

Inflation — the gradual rise in the price of goods and services — averages around 5 to 8 percent per year in many developing countries. If your savings account gives you 3 to 4 percent annual interest, you are actually losing purchasing power every year. The Rs. 100,000 you save today will buy less in ten years than it does right now.

Investing is the antidote to inflation. A well-invested portfolio can grow at 10 to 15 percent or more annually over the long term, far outpacing inflation and building real wealth.

- THE MAGIC OF COMPOUND INTEREST

Albert Einstein reportedly called compound interest the “eighth wonder of the world.” Whether or not he actually said it, the sentiment is absolutely true.

Compound interest means earning returns not just on your original investment, but also on the returns you have already earned. Over time, this creates a snowball effect where your wealth grows faster and faster.

Here is a simple example:

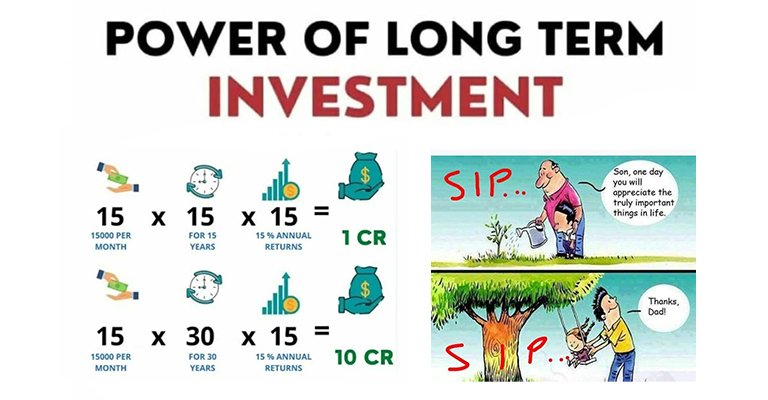

- If you invest Rs. 10,000 per month starting at age 25, at an average return of 12% per year, by age 55 you would have approximately Rs. 3.5 crore.

- If you wait until age 35 to start the same investment, you would have only around Rs. 1 crore by age 55.

Same monthly amount. Same return rate. A difference of Rs. 2.5 crore — simply because of ten years. Time is the most powerful force in investing. The earlier you start, the less you need to invest to reach the same goal.

- UNDERSTANDING RISK AND RETURN

Every investment carries some level of risk. The general rule is: the higher the potential return, the higher the risk. Understanding this relationship is crucial before putting your money anywhere.

- LOW RISK, LOW RETURN: Government savings schemes, fixed deposits, savings accounts. Your money is safe but grows slowly.

- MEDIUM RISK, MEDIUM RETURN: Bonds, balanced mutual funds, real estate. Moderate growth with manageable risk.

- HIGH RISK, HIGH RETURN: Stocks, equity mutual funds, cryptocurrency. High potential gains but also significant short-term volatility.

The right mix of risk depends on your age, financial goals, and personal comfort level. A 25-year-old can afford to take more risk because they have decades to recover from market downturns. A 55-year-old approaching retirement should prioritize capital preservation.

- COMMON INVESTMENT OPTIONS EXPLAINED

STOCKS

When you buy a stock, you buy a small ownership stake in a company. If the company grows and becomes more profitable, the value of your stock rises. Stocks offer the highest long-term returns of any asset class but can be volatile in the short term. Suitable for patient, long-term investors.

MUTUAL FUNDS

A mutual fund pools money from thousands of investors and uses it to buy a diversified portfolio of stocks, bonds, or other assets. A professional fund manager makes the investment decisions. Mutual funds are ideal for beginners because they offer diversification and professional management with relatively small investment amounts.

REAL ESTATE

Buying property — whether residential or commercial — is a time-tested investment in South Asia. Real estate provides rental income and capital appreciation over time. The downside is that it requires significant capital upfront and is not easily liquidated.

GOLD

Gold has been a store of value for thousands of years. It tends to hold its value during economic crises and inflation. However, gold does not generate income like stocks or rental property. It is best used as a small portion of a diversified portfolio as a hedge against uncertainty.

FIXED DEPOSITS & GOVERNMENT SCHEMES

These are the safest investment options available. In Pakistan, instruments like National Savings Certificates offer guaranteed returns backed by the government. They are ideal for conservative investors or for money you cannot afford to lose.

- DIVERSIFICATION: DO NOT PUT ALL EGGS IN ONE BASKET

The most important rule of investing is diversification — spreading your money across different types of assets. When one investment goes down, others may go up, balancing your overall portfolio.

A simple diversified portfolio might look like this:

- 50% in stocks or equity mutual funds (long-term growth)

- 25% in bonds or fixed income instruments (stability)

- 15% in real estate or REITs (passive income)

- 10% in gold (protection against inflation)

Diversification does not guarantee profits, but it significantly reduces the risk of catastrophic loss.

- COMMON INVESTING MISTAKES TO AVOID

WAITING FOR THE PERFECT MOMENT

Many people wait for the “right time” to invest. The truth is, the best time to invest is always as soon as possible. Trying to time the market perfectly is a strategy that even professional investors fail at consistently.

PANIC SELLING

Markets go up and markets go down. When prices fall sharply, fear drives many investors to sell at a loss. This is almost always the wrong move. History shows that markets recover over time. Patient investors who stay invested through downturns almost always come out ahead.

FOLLOWING THE CROWD

Investing in something just because everyone else is — whether it is a hot stock, a trending cryptocurrency, or a real estate bubble — is a recipe for disaster. By the time the general public hears about an opportunity, the smart money has often already moved on.

IGNORING FEES

Investment fees may seem small, but over decades they can consume a significant portion of your returns. Always understand the fees associated with any investment product before committing your money.

- HOW TO START INVESTING WITH SMALL AMOUNTS

You do not need a large sum to begin investing. In fact, starting small and building the habit is far more important than waiting until you have “enough” money.

Steps to get started:

Step 1 — Clear high-interest debt first. Paying off debt with 20%+ interest is guaranteed return.

Step 2 — Build a 3-month emergency fund in a savings account.

Step 3 — Open an investment account with a registered broker or mutual fund company.

Step 4 — Start with a small, regular monthly investment — even Rs. 2,000 to 5,000 is a beginning.

Step 5 — Reinvest all returns and dividends. Let compounding do its work.

Step 6 — Review your portfolio every 6 months and rebalance if needed.

Consistency beats perfection every time.

CONCLUSION

Investing is not a privilege of the wealthy — it is the path to becoming wealthy. The principles are simple: start early, diversify, stay patient, and let compound interest do the heavy lifting over time.

Every great financial journey begins with a single step. You do not need to understand everything before you begin. You just need to begin. The knowledge will follow. The results will follow. And one day, you will look back and be grateful that you started when you did.